Cheli : Guruji, I have heard that GST department is initiated conducting audits. State GST department has identified some dealers, who shall be audited by the department. Is it true?

Guruji : Yes, It is true. Both the Central & State GST department has identified some dealer who shall be audited by the department.

Cheli : But I’m afraid, If I being audited by them. My books of accounts are already audited by the Chartered Accountants twice under Companies Act, Income Tax and GST Act too. Is this audit is different than these audits.

Guru ji : Yes, It is different than the audit conducted by the Chartered Accountants, Lets me explain you in detail.

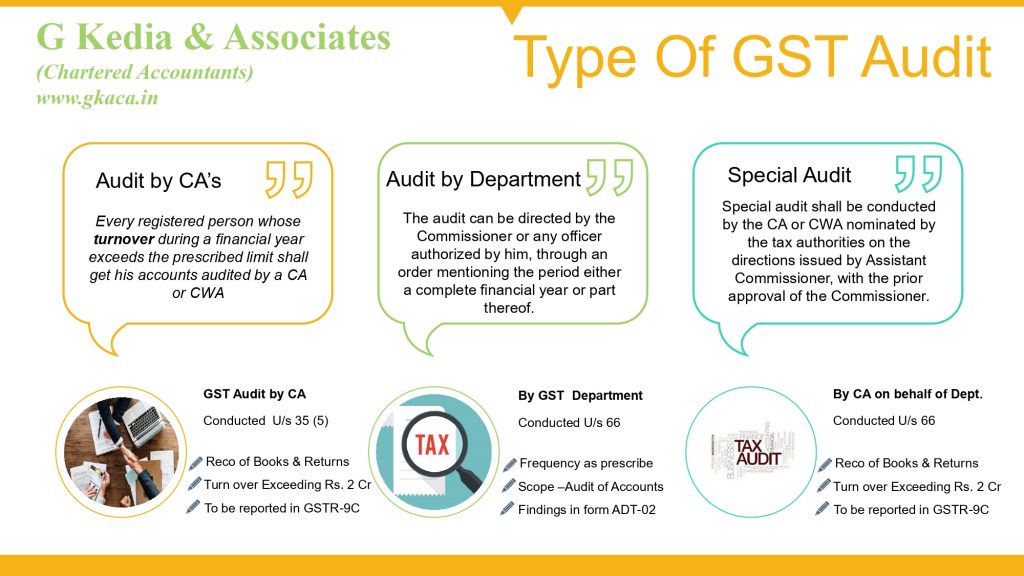

Type of Audit under GST law

Procedure of Department GST Audit

1) The RP shall be informed by way of a notice in FORM GST ADT-01, not less than fifteen working days prior to the conduct of audit in such manner as may be prescribed.

2) The audit shall be completed within three months from the date of commencement of the audit which could be extended in writing upto six months. The “commencement of audit” has been prescribed as the date on which the records /other documents, called for by the tax authorities, are made available by the RP or the actual institution of audit at the place of business, whichever is later.

3) During the course of audit, the officer may require the RP (i) to afford him the necessary facility to verify the books of account or other documents; (ii) furnishing such information as he may require; and (iii) render assistance for timely completion of the audit.

4) On conclusion of the audit, the proper officer shall, within thirty days, inform the RP the findings of audit in FORM GST ADT-02, with the findings and the reasons for such findings.

5) The authorized officer shall conduct the audit of the records and the books of account of the RP, verify the documents on the basis of which the books of account are maintained, verify the returns and statements furnished, the correctness of the turnover, exemptions and deductions claimed, the rate of tax applied, the ITC availed and utilized refund claimed, and other relevant issues and record the observations in his audit notes.

Details/documents to be kept ready by the taxpayer

Following documents are required to be furnished by the taxpayer for the purpose of Departmental Audit under GST:-

| 1. | GSTR-1, GSTR-2A, GSTR-3B, GSTR-9 and GSTR-9C and their respective reconciliations | |

| 2. | GST Registration Certificate | |

| 3. | Copies of Annual Report, Auditor’s Report, Trial Balance for the audit period | |

| 4. | Income Tax Returns along with Annexure (Form 3CA/ 3CD and 3CEB) if any, for the audit period | |

| 5. | Returns if submitted to Banks/ Financial Institutions for the Audit Period | |

| 6. | Cost Audit, Tax Audit and Internal Audit reports, wherever applicable for the audit period | |

| 7. | Electronic Credit and Cash Ledger | |

| 8. | Abstract of output invoices of taxable, NIL Rated, exempted and zero rated supplies, wherever applicable for the audit period | |

| 9. | Abstract of input invoices for the audit period | |

| 10. | Work orders/purchase order/ agreements for the audit period | |

| 11. | Duly filled in GSTAM (GST Audit Manual) Annexure-I/V and VI | |

| 12. | Copy of last general audit report |

This list of documents is not exhaustive and has been compiled on the basis of notices issued to the taxpayers. However, the department can demand any other details which it may consider necessary for audit depending on facts and nature of transaction of the taxpayer.

Challenges in GST Audit

a) Most of the authorities call for submission of long list of readily available list of records from the RP without citing any reason for the same. As the entities are filing returns, both monthly as well as annual returns with due certifications by an authorized chartered accountant or cost accountant, most of the information and records exists and is available in digital form with the authorities. Some of the records called for includes: Invoices, debit notes, balance sheet, GSTR 1 etc. which are digitally accessible by all authorities concerned from the credible source. The present practice of routinely calling for list of records with no reasons cited is an opaque start for conduct of audit. It becomes a tool of harassment by the authorities, which should be avoided.

b) When the authorities are in possession of such information and records, calling for the same from the RP appears to be an undesirable activity. Instead, the officers should be asked to conduct audit using the digital data / records available in the systems and for any discrepancy they can call the RP to produce specific records in writing, after due approval of a senior officer of the rank of Commissioner, citing the reasons for verification of such records or information. The timely verification of the records and data available with the departments is of utmost importance as auditors are supposed to verify the records maintained for the purposes of compliance with GST laws and is readily accessible to the authorities concerned. This could be done regularly by officers of audit in their offices without the need of the RP to attend. Therefore, in the changed situation, in majority of the instances, all necessary verifications could be conducted in the office itself, the author feels.

c) As the audit could be carried out using digital tools, all officers of audit should be mandated to undergo a requisite training, get certified and then allowed to resume audit. This needs to be strictly adhered to as most of the officers are not equipped, both technologically as well as legally, for the specialized task.

d) There is a need of specific tailor-made programme in place for this purpose with standard operating mechanism. It should be ordered that only officers, including those in senior posts, duly qualified as above and certified, will be posted for audit. As on date, we have data fully available but the manpower is totally under-prepared for the assigned task as they do not know the method to be followed. This gap at the back-end should be covered first before allowing the audit, so that unnecessary harassment to the RP could be minimized.

e) The unskilled audit officer (both in digital and legal analysis) may not be in a position to observe any deviations that may result in loss of revenue to the exchequer. By adopting the present un-organised varied approach of audit, the department may not be in a position to notice and plug the possible revenue leakages in an effective manner.

f) When audit is being conducted after due analysis of in-house data as suggested, identifying the issues to be audited, the notice/intimation for audit could be sent asking for the specific documents/information only with reasons duly recorded. Later, if required, the officers should be allowed to visit the business premises with specific verification tasks assigned in writing.

g) In cases where the audit, after due specific analysis, are conducted at the GST offices, the Authorities expect the RP to be available at the office when they undertake the audit process, which could be avoided. The RP finds it difficult to assign an employee exclusively for this purpose for many days to the office. Instead, the officers should be asked to communicate in writing the issues that require further clarification by mail and also call for the visit personally for clarifying the required issues.

h) There is no uniform approach or SOP prescribed for the officers to conduct audit at the backend. Each authority follows one or more methods of conducting of audit, depending upon their own understanding of law and compliance requirements. This has caused huge problems to the RP as each officer has his own plans and procedure and it becomes difficult to respond immediately in a fair manner. Also, the person in-charge of accounts may not be aware of all the happenings of large entities. There is need of SOP for conduct of audit by the executives and it should be notified to all stakeholders, so that there is transparency in place.

i) The CBIC has come out with an Audit Manual which is a replica of the erstwhile EA-2000 audit methodology, applied to large manufacturing units in central excise tax regime. It is a matter of fact that this procedure is not followed even by all the central authorities, who change the system according their own understanding. Further, it is also a matter to be considered as to how the audit procedures for an origin based tax system could be useful to the changed times of consumption based tax regime.

j) Added to this, the state authorities are not following the said standards as this manual is not tailor-made for the GST regime. Now the larger issue for the RP is how to comply with these varieties of requirements from different authorities. This needs to be set right on priority or else it will compete with the same opaque system which existed earlier, with no useful change on the ground situation and results

Precautions for assessee

With the issue of notices for GST audits, it can be rightly said that the era of departmental audit has begun. Since, this is the first time that the audit under GST regime is being initiated, it is going to be another challenge for the department as well as taxpayers. Verification of abovementioned documents in detail, to check the accuracy of output taxes, input tax credit, refunds and other aspects may take extra time for completion of audit.

In order to ensure that the process of audit goes smoothly and to avoid unnecessary harassment by the department, the taxpayers need to prepare themselves for such audit. They should start collecting relevant details and documents and reconcile the same to prevent last minute chaos. Even though, the department will specify in the notice documents and information it needs from taxpayers, still it is suggested to the taxpayers to consolidate their data on the basis of list of abovementioned documents.

Conclusion

In pre-GST regime also, the department had conducted audit whether in Excise or VAT or Service Tax. In view of the numerous amendments and modifications carried out in the Act, Rules, GST rates, etc., the new indirect taxation regime has still not achieved stability. The taxpayers are finding it difficult to run their businesses along with managing GST compliances. On the top of that, if audit is not undertaken in a fair manner, the taxpayers will suffer from great amount of hardship.

Therefore, the department should give fair chance to assessee in bonafide cases and should not straightaway impose penalty and proceed with prosecution

CA. Gopal Kedia