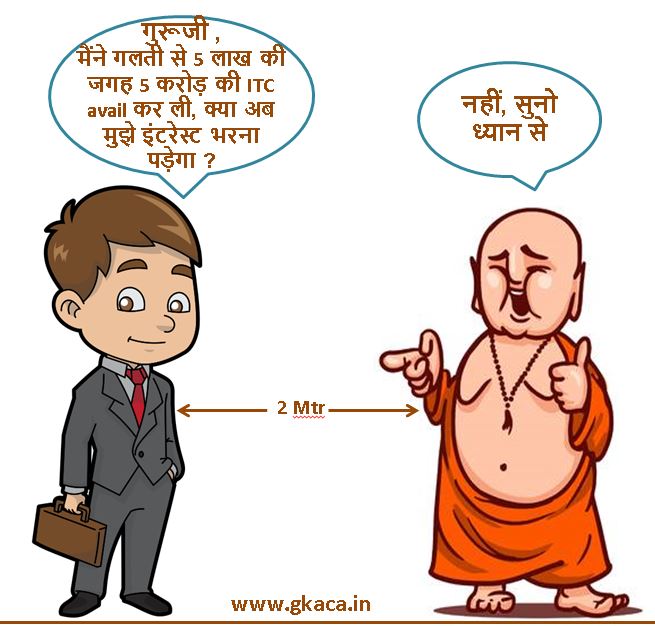

Chela : Guruji, While filing GSTR-3B for the month of January 2020, My accountant has made some typographical error and avail ITC of Rs. 5.00 crore instead of Rs. 5.00 lakh. Though I have not utilised such ITC against payment of my output tax liability. Do I have to pay interest on such un-availed ITC?

Guru ji : No, Not required

Chela : But I went to Google baba, He said, Hon’ble Supreme court in case of – Ind-Swift Laboratories Ltd. — 2011 (265) E.L.T. 3 (S.C.), held that interest on such un-utilised ITC is required to be paid.

Guru ji : बेटा, तो फिर तुम मेरे पास क्यों आये हो |

Chela : for 2nd opinion

Guruji : Then keep the 1st opinion aside and listen it.

Is SCN compulsory to collect the Interest U/s 50 ?

At the outset it is pertinent to note that, sec 50 of GST Act using the term, ‘on his own‘ which means the interest payable under section 50 shall be payable by the registered person on his own. In case recovery proceeding initiated by the department then, it sho uld be routed through the adjudication process. Recent judgments of the various high courts suggests that, one thing is very much clear that the adjudication/quantification of liability is prerequisite for initiation of recovery proceeding. The honorable high courts has taken view that the even though the chargeability of the interest has been automatic even but the quantification of the interest liability is utmost necessary.

One must appreciate the wording of the judgment of honorable of Madras High Court in the case of Assistant Commissioner of CGST & Central Excise v. Daejung Moparts (P.) Ltd. [2020] 116 taxmann.com 372 (Mad.)

that “quantification of such liability certainly needs an arithmetic exercise after considering the objections if any, raised by the assesse. It is to be noted that the term “automatic” does not mean or to be construed as excluding “the arithmetic exercise. Therefore, in my considered view, though the liability of interest under section 50 is automatic, quantification of such liability shall have to be made by doing the arithmetic exercise, after considering the objections of the assessee.” So by these wordings the honorable high court clearly set out the principle that the arithmetic exercise to quantify the interest liability is something which is primary requirement before going into the recovery proceedings and the same is to be carried out in accordance with and the manner provided by the Sec 50(2) read with prescribed rule which is yet to be notified by the government.

Does the Sec 50 has power to collect the Tax on Un-utilised ITC

Interest under section 50 of GST law cannot be collected mere on the ground that ITC is reflecting in electronic credit Ledger, where such ITC is never utilized for payment of Taxes, the provision contained in section 50 are reproduce herein under,

50 . (1) Every person who is liable to pay tax in accordance with the provisions of this Act or the rules made thereunder, but fails to pay the tax or any part thereof to the Government within the period prescribed, shall for the period for which the tax or any part thereof remains unpaid, pay, on his own, interest at such rate, not exceeding eighteen per cent, as may be notified by the Government on the recommendations of the Council:

[Provided that the interest on tax payable in respect of supplies made during a tax period and declared in the return for the said period furnished after the due date in accordance with the provisions of section 39, except where such return is furnished after commencement of any proceedings under section 73 or section 74 in respect of the said period, shall be levied on that portion of the tax that is paid by debiting the electronic cash ledger. ]

(2) The interest under sub-section (1) shall be calculated, in such manner as may be prescribed, from the day succeeding the day on which such tax was due to be paid.

(3) A taxable person who makes an undue or excess claim of input tax credit under sub-section (10) of section 42 or undue or excess reduction in output tax liability under sub-section (10) of section 43, shall pay interest on such undue or excess claim or on such undue or excess reduction, as the case may be, at such rate not exceeding twenty-four per cent, as may be notified by the Government on the recommendations of the Council.

The first sub section (1) would covering the scenario where there is a shortfall in payment of tax which inter alia may be on account of payment of tax using irregularly availed credit. In other words, there may be short payment of tax by utilization of ineligible credits. Mere availment of credit, without utilization, may not fall within the scope of this provision, as it would get triggered only due to failure to pay the tax

The sub section (2) is extension of the sub section (1), which basically provides the mechanism to calculate the interest under sub section (1). The term ‘prescribed’ has been defined in section 2(87) of the CGST Act, 2017 and accordingly prescribed means as prescribed by the rules. It is interesting to note that even as of now no rules has been prescribed for the purpose and manner in which the interest u/s 50 should be calculated. So the moot question is that if the law itself not provided the manner how the interest is to be calculated u/s 50 and then the applicability of the whole section comes under question. Mere providing of the rate of interest would not be sufficient to trigger the interest. Therefore in absence of machinery provision for collection of interest the whole levy under section 50 (1) fails. Presently this position has not been challenged in the court of law therefore this need to be tested with time.

The scope of sub-section (3) is restricted to cases falling under sub-section (10) of Section 42 & 43. Section 42 & 43 relate to matching, reversal and reduction of ITC and output tax liability respectively. This provision doesn’t cover a scenario wherein an ineligible credit has been availed by an assessee for reasons other than that of mismatch of credit. In the case under discussion, the said disallowance of ITC not on account of matching and mismatching of ITC in GST returns. Therefore the interest under sub section (3) cannot be levied on such excess availment of ITC.

Further in respect of actual mismatch cases also, interest under sub section (3) cannot be levied in the absence of the non-availability of returns, the provision itself is unworkable and hence, there would be no requirement to levy the interest.

Does the Proper officer is empowered to collect Interest under Sec 73 / 74

Further, we herewith would like to discuss the provision of recovery provided in sec 73 of GST Act. Section 73 of the CGST Act, 2017 contains the machinery provision which empowering to demand irregularly availed credit. For better appreciation of the legal issue involved, this provision is reproduced below: –

Where it appears to the proper officer that any tax has not been paid or short paid or erroneously refunded, or where input tax credit has been wrongly availed or utilized for any reason, other than the reason of fraud or any willful misstatement or suppression of facts to evade tax, he shall serve notice on the person chargeable with tax which has not been so paid or which has been so short paid or to whom the refund has erroneously been made, or who has wrongly availed or utilised input tax credit, requiring him to show cause as to why he should not pay the amount specified in the notice along with interest payable thereon under section 50 and a penalty leviable under the provisions of this Act or the rules made thereunder;.

As per the above provision, the proper officer can issue a notice for wrongly availed credit and demand interest only where interest is payable under Section 50. Sec 73 doesn’t have authority to levy the interest, a careful examination of said section suggest that sec 73 borrows authority form sec 50 of the Act to collect the interest on irregular ITC.

From the discussion supra, it can be said that Section 50 does not provide for payment of interest for mere wrongful availment of credit. Once there is no interest payable under section 50, the CGST Act does not provide for a provision to demand interest in cases where availment of credit is irregular.

At this juncture, reference can be made to the settled jurisprudence on this issue. In India Carbon Ltd. v. State of Assam, [(1997) 6 SCC 479], the Supreme Court was examining whether the provisions of the CST Act authorized imposition of interest for delayed payment of central sales tax. Based on the relevant provision, as it existed during that time the Court held that the provision relating to interest in the latter part of Section 9(2) can be employed by the States’ sales tax authorities only if the Central Act makes a substantive provision for the levy and charge of interest on central sales tax. The principle which one can infer from this decision is that unless the law clearly provides for a provision for recovery, no interest can be recovered.

As the provisions relating to recovery of interest under CGST Act does not envisage the scenario of irregular availment of credit, it appears there cannot be any levy of interest on mere wrongful availment of credit for reasons other than those covered under Section 50(3) viz. wrongful availment on account of mismatch.

In support of our argument we would like to place our reliance on below case laws,

In case of M/s Commercial Steel Engineering Vs State of Bihar (Patna High Court) Civil Writ Jurisdiction Case No.2125 of 2019 dated 27/06/2019, it is quoted,

“ Had it been a case where the credit shown in electronic ledger, was availed or utilized for meeting any tax liability for any year, there would be no error found in the action complained but it would be stretching the term ‘availment’ beyond prudence to treat the mere reflection of the transitional credit in the electronic credit ledger as an act of availment, for drawing a proceeding under section 73(1) of ‘the BGST Act’. The provisions underlying Section 73 is self eloquent and it is only if such availment is for reducing a tax liability that it vests jurisdiction in the assessing authority to recover such tax together with levy of interest and penalty under section 50 but until such time that the statutory authority is able to demonstrate that any tax was recoverable from the petitioner, a reflection in the electronic credit ledger cannot be treated as an ‘availment’.

The legislative intent reflected from a purposeful reading of the provisions underlying section 140 alongside the provisions of section 73 and Rules 117 and 121 is that even a wrongly reflected transitional credit in an electronic ledger on its own is not sufficient to draw penal proceedings until the same or any portion thereof, is put to use so as to become recoverable. “

Hon’ble Karnataka High Court – BILL FORGE PVT. LTD 2012 (279) E.L.T. 209 (Kar.) hold that Assessee had not taken benefit of wrong entry in their account books, there was no liability to pay interest – Once entry was reversed, it is as if that Cenvat credit was not available or NOT TAKEN at all. Therefore provision of Rule 14 of CENVAT credit rules, 2004 will not apply for charging interest on such ITC. Hon’ble High Court distinguished judgment of .

Hon’ble High Court ruled that words used in Rule 14 of Cenvat Credit Rules, 2004 are ‘taken’ or ‘utilized wrongly’, and not ‘avail’ – If before utilization of credit, entry has been reversed, it amounts to not taking credit on inputs. Interest is compensation to Revenue and imposed on assessee who had withheld payment of tax as and when it was due and payable – Delay beyond date when duty is payable deprives Revenue of the duty, and said amount is in possession of assessee who would have its benefit – Its levy is on actual amount which is withheld and extent of delay in paying tax on due date – If there is no liability to pay duty/tax, there is no liability to pay interest.

Therefore merely taking wrong ITC would not result into Levy of interest until output tax gets short paid due utilising such wrong ITC. Interest may trigger only when there is short payment of output GST liability.

Conclusion

Apart from the technical discussion, It is logical to understand that where exchequer is not incurring any loss hence question of compensation by way of interest doesn’t arises.

CA Gopal Kedia

Though it is HARD TO believe but it seems to be True.

The Credit is said to be TAKEN only when it is used for paying TAXES, if it remains as CREDIT and reversed before being used, it should be DEEMED as not taken in first place itself. Hon’ble Karnataka High Court in Bill Forge Pvt Ltd – 2012 (279) E.L.T. 209 (Kar.) dismissed departments appeal by distinguishing Hon’ble SC judgment in Ind-Swift Laboratories Ltd. — 2011 (265) E.L.T. 3 (S.C.). This lead government to change the Rule 14 of Cenvat Credit Rules w.e.f 1-4-2012 to state that interest will be payable only when the CENVAT credit wrongly TAKEN was UTILIZED too. Merely taking wrong CREDITS will not attract interest. Therefore merely taking wrong GST-ITC in electronic credit ledger will not result into interest liability unless it is utilized too . By using wrong ITC we SHORT pay our GST output liability which may attract interest. Subject to availability of METHOD of calculation to arrive at interest payable under such cases.

Further to add to your thought process : Section 50(1)- provides for interest payment on taxes remaining unpaid by the assessee ” on its OWN” @ 18% p.a.

Therefore one must wonder whether Interest under Section 50(1) is not payable at all if the assessee pays upon getting SCN or intimation from department to pay. Interest @ 18% is payable only when the assessee pays it on it free will viz on it OWN. Though the intention of legislature will not be such, but the wordings used by legislature forces us to interpret the law otherwise.

Rule 37 (3) of CGST rules, 2017 specifically provides for method to calculate interest when the recipient fails to pays its supplier within 180 days from date of issue of GST invoice. It states rate specified under Section 50 (1) will be applied for the period starting from date of availing credit on such supplies till date when the amount is added to output liability is paid.

But how to calculate the interest in general cases is not specifically given in CGST Rules, 2017. Whether we are missing something crucial or this is intentional omission which needs to be understood by IMPLICATION only time will tell. Courts will be flooded with similar questions in times to come. One should buckle up to be ready to fight the WAR which will be imposed on industry by GST.